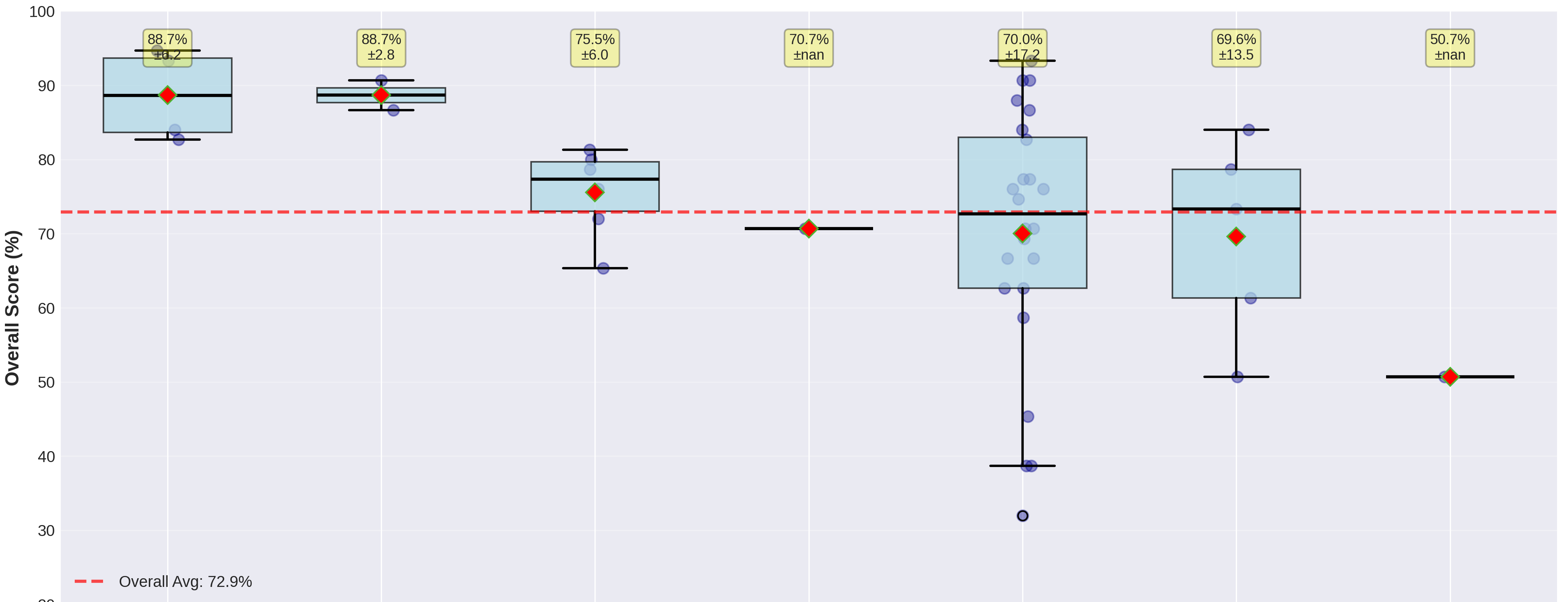

1. Where do we stand on customer experience across regions?

The overall average score is 72.9%, which sets a reasonable baseline across stores in Malaysia. George Town (Penang) and Melaka stand out clearly, both averaging 88.7%, with all stores in these locations performing consistently well. These two locations show what strong execution looks like and can be used as internal benchmarks for other regions.

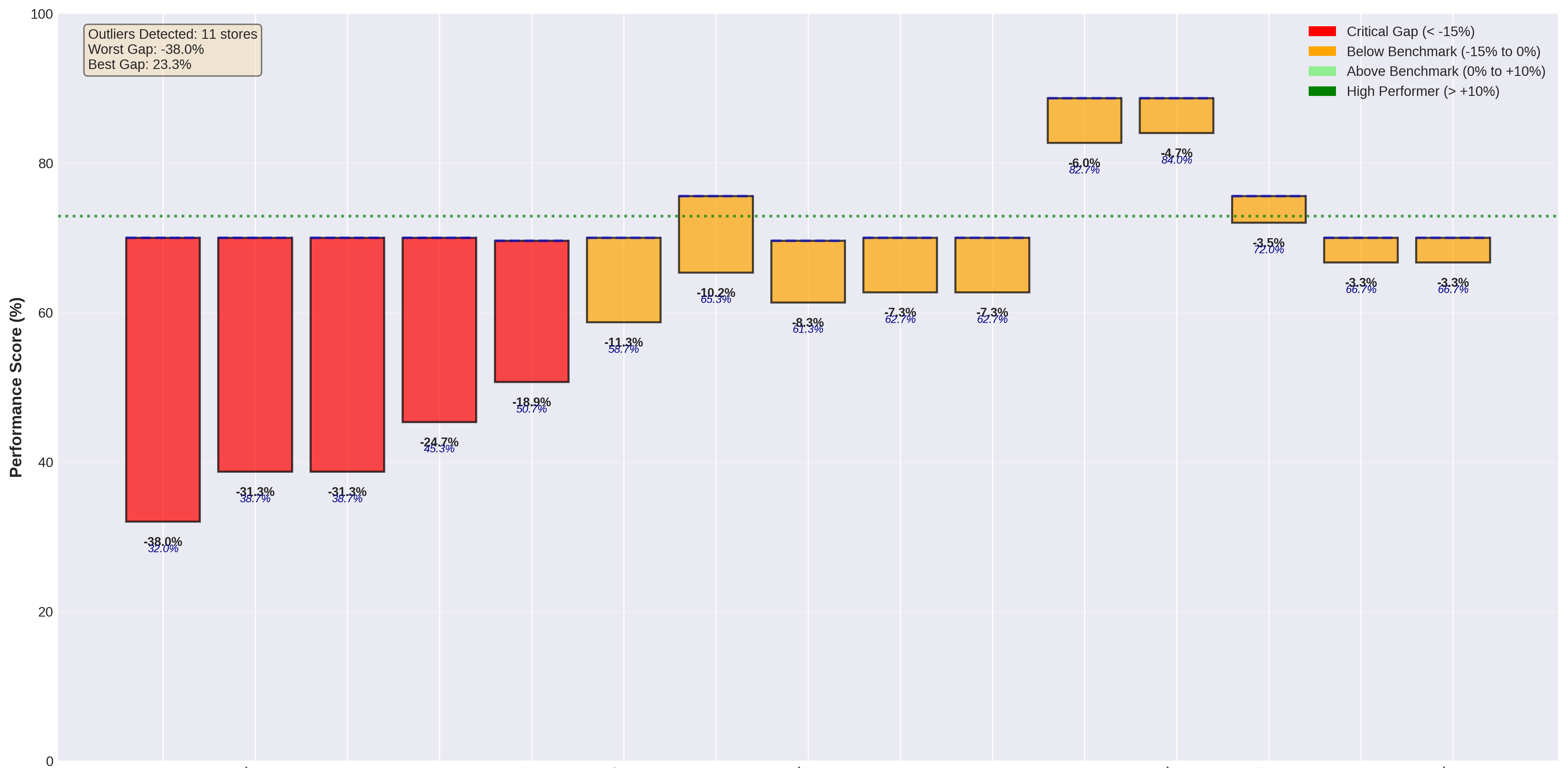

Most other locations sit around the acceptable range. Petaling Jaya (75.5%) and Ipoh (70.7%) are broadly stable, while Kuala Lumpur (69.6%) and Other Locations (70.0%) fall slightly below the overall average. The bigger concern is inconsistency, especially within the "Other Locations" group, where store scores range from 93.3% down to 32.0%, suggesting uneven standards rather than a single shared issue. Kota Bharu, represented by a single store scoring 50.7%, is clearly underperforming and requires attention.

In practical terms, stores scoring above 80% are performing well and can serve as examples, 70-80% should be monitored, 60-70% need coaching, and anything below 60% signals the need for urgent action.