Dataset and Methodology

The dataset used for this analysis contains 34,500 retail and e-commerce transactions. It covers 17 fields that track orders, products, revenue, discounts, profit margins, returns, and delivery times. This gives a detailed record of both financial outcomes and operational processes.

Customer demographics, such as age and gender, along with product category information, were also included. These details make it possible to segment results and understand how different groups or product types contribute to performance.

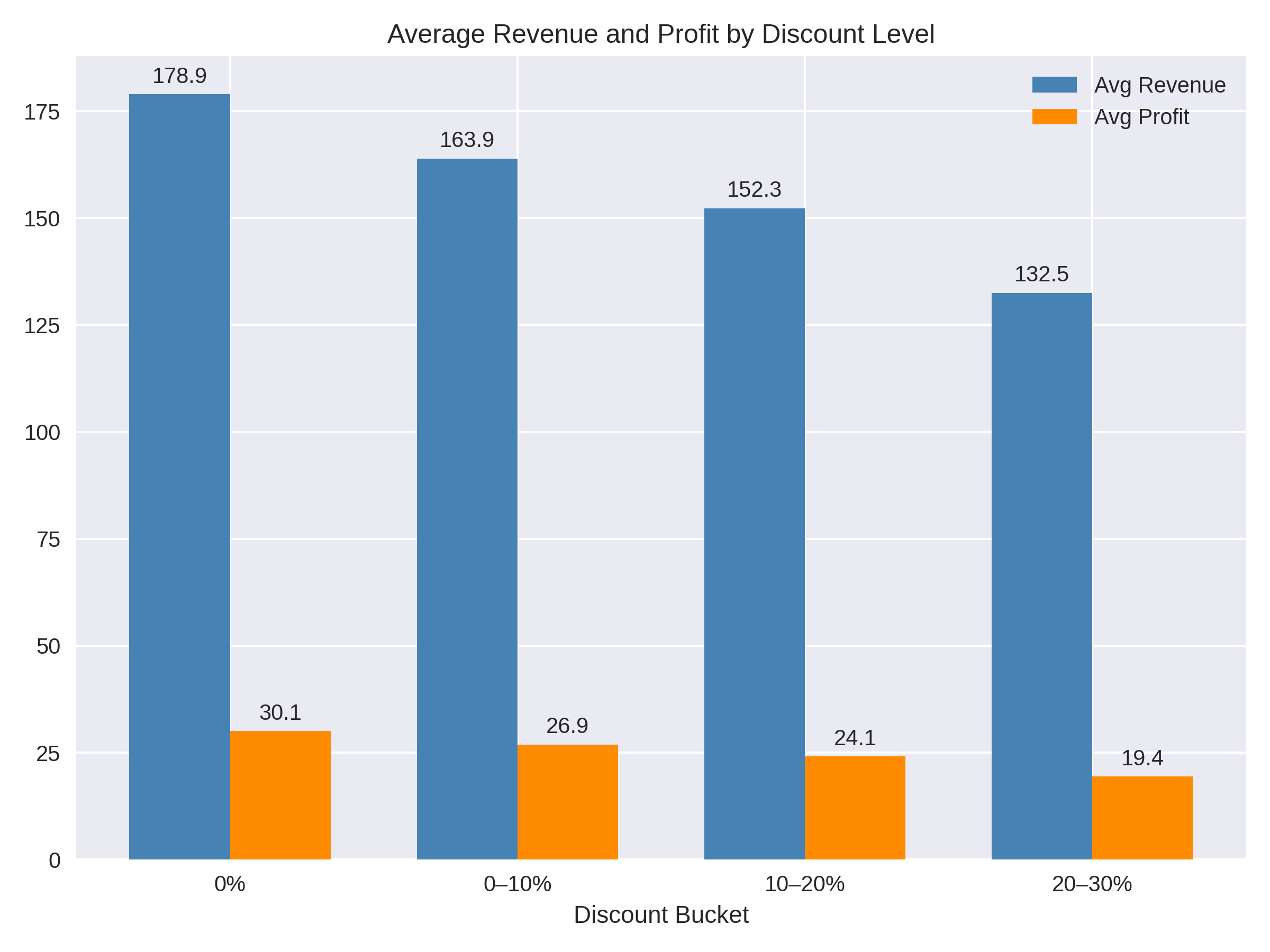

By combining financial, operational, and demographic data, the dataset provides a full picture of store performance. It allows us to measure revenue drivers, evaluate the effect of discounts on profit, and identify where issues such as high return rates or delivery delays impact results.